The Chancellor delivered his Autumn Budget on 22nd November, setting out the Government's tax policy for the next fiscal period. Forewarned of a "balanced approach", the proposed capital gains tax (CGT) changes for non-residents investing in commercial property came as a surprise. However, a welcome announcement for first-time buyers was made, exempting stamp duty land tax on the first £300,000 of the purchase price, provided the price itself is under £500,000.

Capital gains

From April 2019, the Government intends to bring non-UK residents within the scope of UK corporation tax or CGT on gains arising on the disposal of UK commercial property. Important features of the new rules include:

- The new rules will apply a single, unified regime to both UK residents and non-UK resident investors.

- There will be a valuation "rebasing" of interests in UK commercial properties held by non-residents from April 2019 (so historic gains will not be subject to the new tax). Note that there will be the option to disapply these rules on direct property sales if rebasing would give rise to a worse result.

- The new rules will apply to both the direct disposal of UK property, but also the disposal of indirect interests in UK property. This will include the sale of a "property rich" company by a person (or connected persons) who have at least a 25% interest in that company. A "property rich" company will broadly be one where 75% or more of its gross value at disposal is represented by UK property.

- For so-called indirect disposals, there will be a reporting requirement for the non-resident investor's UK advisers, who must report a sale to HMRC within 60 days (unless they are reasonably satisfied that the non-resident has reported it).

- The Government will introduce certain "anti-forestalling" rules and a Targeted Anti-Avoidance Rule (TAAR) to give the changes more teeth.

The current CGT exemption for non-UK resident investors in UK commercial property has long since been under siege, given the annual raft of changes to the UK tax code governing UK residential real estate. The Government has now decided to kick the front door in from April 2019. These are major changes: non-resident investors in UK commercial property will have to factor in UK tax on capital gains arising on disposals from April 2019. The proposals are still being consulted on, but the Government has made it clear that the core aspects of these changes are going to come into force, so it is only really consulting on the detail.

It is not only non-UK resident investors in commercial property who will be hit. For example, the current CGT regime for residential property provides an exemption for "widely held" non-resident companies – this carve out will be removed as owners of residential property in those circumstances will simply be subject to the same rules as those owning commercial property. Will the changes make the UK less attractive? The answer is clearly yes from a tax point of view, but the impact on behaviour will remain to be seen. Will it drive more investors onshore, in search of tax efficient vehicles? For example, Real Estate Investment Trusts and PAIFs will be extremely attractive vehicles, assuming that the Government does not seek to tinker with the tax benefits associated with their ring-fenced property investment businesses. Certainly, many tax exempt investors in entities such as Jersey or Guernsey domiciled unit trusts may look to restructure their holdings going forward, given that these unit trusts may be tax-inefficient for such investors from a CGT perspective from 2019.

Non-resident landlords to be brought within the scope of corporation tax?

The Government has stated that it will publish a response to the consultation on bringing non-resident companies within the scope of corporation tax on their property income "shortly after the Autumn Budget".

Bringing non-resident landlords within the scope of corporation tax, rather than income tax, at first sight sounds favourable. After all, corporation tax is lower at 19%, falling to 17%, compared with 20% income tax. Unfortunately, recent changes to the corporation tax rules mean that this decision, to be consulted on further next year and taking effect from 6 April 2020, could increase the net tax from UK property receipts. This is because companies paying corporation tax can be restricted on the amount of interest and other finance costs they can deduct beyond the restrictions applicable to income tax payers. In addition, companies paying corporation tax can be subject to the hybrid rules if, as is common in some structures, individual entities or interests in entities have different tax treatment in different countries. This decision is consistent with other measures, whether announced in earlier Budgets or this Budget, to equalise the tax take from UK activities irrespective of how the assets are held or financed. It may mean that, in due course, corporate taxpayers and their advisers may not have to be so concerned about the Non-Resident Landlord Scheme and withholding from rent, if HMRC is more confident that corporation tax can be collected. This proposal forms part of a wholesale revision of the tax treatment of UK property (for example, the extension of capital gains tax to non-UK resident investors in commercial property).

There are a number of miscellaneous changes to SDLT which were announced in the Spring Budget 2017.

First-time buyers

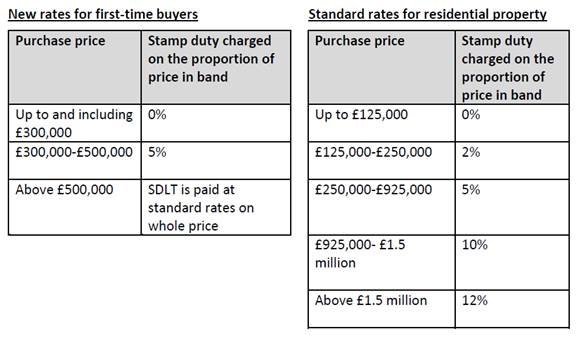

The Government has extended the stamp duty land tax (SDLT) relief for first-time buyers of residential property with a value up to £500,000.

The relief will mean that first-time buyers purchasing homes intended to be their only or main residence:

- up to £300,000 will benefit from a new 0% rate of SDLT, and

- between £300,001 and £500,000 will be subject to a 5% rate on any sums over £300,000.

A comparison of the new rates with the "standard" residential rates is set out below:

This is a welcome change for those falling within the definition of "first-time buyer". This definition will broadly mean someone who has never owned an interest in any residential property anywhere in the world at any time. The maximum saving will be £5,000.

Changes to 3% additional rate for residential property

As announced at the Autumn Budget 2017, the Government has stated that it will legislate in the Finance Bill 2017-18 to make some minor amendments to improve the operation of the 3% SDLT surcharge for additional residential properties by granting relief in certain cases where:

- a court order issued on a divorce or dissolution of a civil partnership prevents someone from disposing of their interest in a main residence;

- an individual buys property from their spouse;

- a person buys a property in a child’s name or on a child’s behalf, where they are doing so in their capacity as the deputy of that child; or

- a purchaser adds to their interest in their existing main residence.

These changes will take effect from 22 November 2017.

The relief noted at point 4 above is particularly helpful as it gives relief from the surcharge for the price paid for lease extensions on a main residence, which was one of the more unfair applications of the rules. However, the draft legislation shows that this relief will be subject to certain carve outs, including where the existing interest is a lease with a remaining term of less than 21 years.

14-day SDLT filing and payment window

The Government has confirmed that the SDLT filing and payment window will be reduced from 30 days to 14 days, applying to land transactions with an effective date on and after 1 March 2019. The new time limit will be onerous for professional advisers, particularly on larger scale portfolio transactions. The only plus point is that the Government is planning improvements to the land transaction return to make compliance with the new time limit easier. Legislation will be introduced in Finance Bill 2018-19.